How to Insure Gold Bullion: A Step-by-Step Guide for Investors

July 14, 2025

Key Takeaways

- Review and compare insurance options, including existing policies, riders, and standalone coverage.

- Document your gold holdings thoroughly for accurate valuation and claims.

- Select a secure storage solution and carefully review all related contracts.

Precious metals are famously used as safe-haven assets that safeguard one’s portfolio from stormy economic weather. Unlike intangible financial instruments like stocks, bonds, and fiat currency, gold tends to retain its value and even perform well in otherwise unfavorable market conditions, like recessions and periods of inflation.

However, physical holdings do come with inherent vulnerabilities. Theft, damage, and loss can be financially devastating if you don’t insure bullion. In a worst-case scenario, you’ll be glad to have a way to recover the value of your assets.

Follow these instructions, and enjoy peace of mind.

1. Check Your Existing Coverage

Homeowners’ and renters’ insurance policies may provide limited coverage for precious metals and rare coins. However, these policies usually classify them as personal property and may not provide adequate coverage for the full value of your holdings.

For example, a typical homeowners’ insurance policy may cover gold for up to $250. Based on the current spot price of $3,257.40 per ounce, that policy would only cover approximately 0.0767 grams of gold.

Furthermore, these residential policies aren’t suitable for investors who need to insure gold bullion held elsewhere. While precious metal depositories and vaults may offer insurance as part of their service packages, the contents of bank safety deposit boxes aren’t usually covered.

In summary, the first step in learning how to insure gold is to see if you can modify your residential policy to cover the full value (if you store your gold at home) or look into available insurance options at your preferred storage facility.

2. Take Inventory of Your Holdings

Whether you need to adjust an existing policy or take out a new one, you must know the precise value of your holdings and make a clear record of all relevant details. Providing comprehensive information for appraisals and concrete proof of ownership is crucial when making a claim.

Before you insure bullion, take detailed notes of each piece’s date of acquisition, weight, purity, serial number, and any unique characteristics. Take videos and photos for further proof. Gather, photograph, and make backup copies of all receipts.

3. Account for Market Fluctuations

As you determine the overall value of your holdings, remember that your portfolio’s value can change with time. Gold’s value is stable and dependable. However, in large quantities, even slight movements can significantly impact the value of your precious metals portfolio.

“Agreed value” insurance policies only cover a locked-in price based on what you initially paid. It’s crucial to choose a policy that will make you whole based on the gold’s current value at the time of loss.

When you insure gold bullion, be aware that the insurance provider may require that you update your coverage on an ongoing basis to reflect rising values. This may not be necessary for small-scale investors, but larger investments may need updated coverage during market surges.

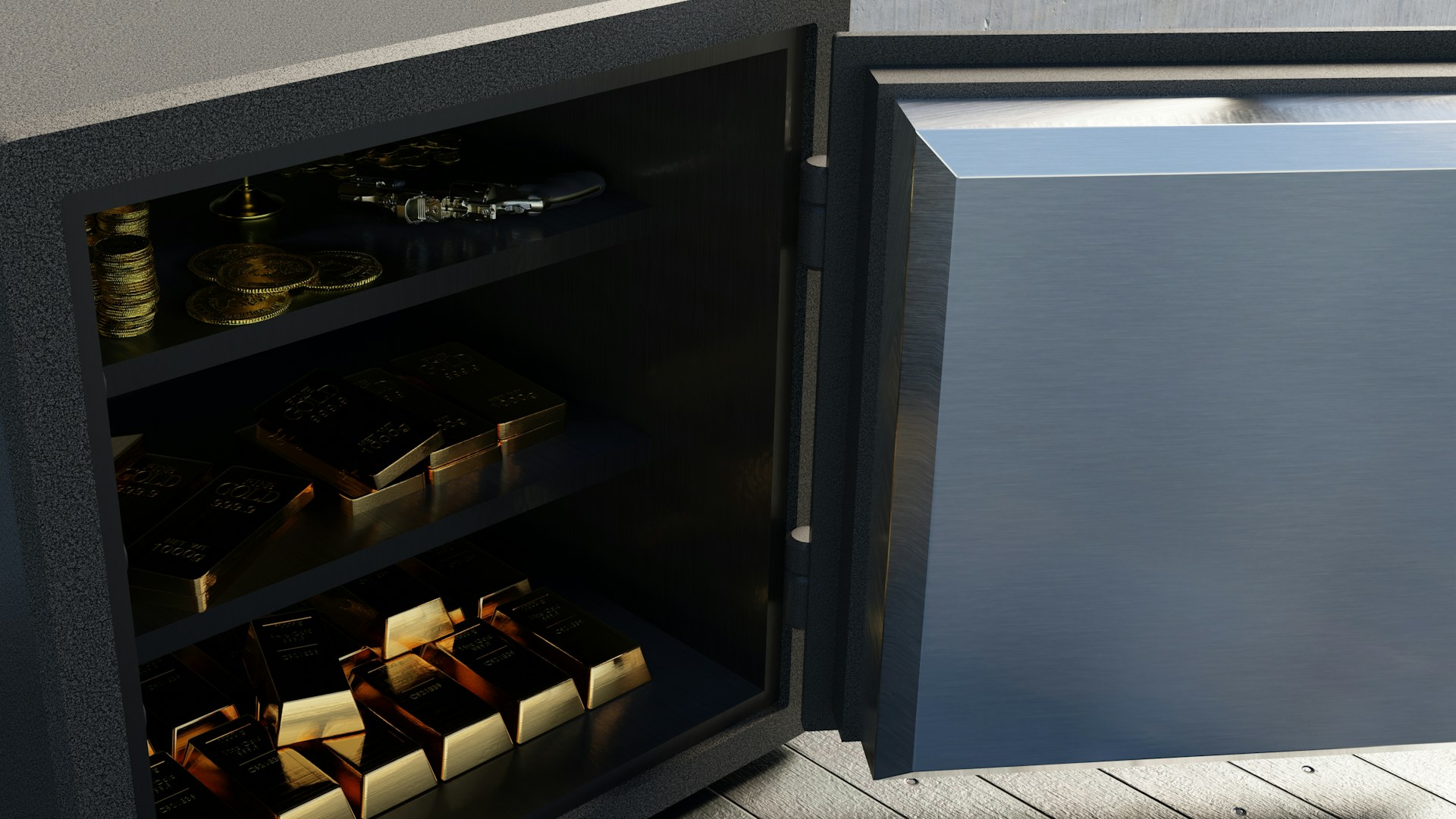

4. Decide on a Storage Solution

Where you store your gold holdings affects how to insure them and the premiums you will pay. In most cases, policies for home storage have higher premiums because the risk of theft, loss, or damage is higher.

Although premiums tend to be lower when you store precious metals at a secure facility, you must also factor the storage fees into the overall expense.

Some depositories and vaults may insure bullion for you. This can be included with the service package or added for an extra fee. Most banks require that you provide your own insurance coverage for items stored in safety deposit boxes.

There’s no single best storage solution. Context matters. In general, large quantities of gold ($10,000+) should be stored in a precious metals depository or vault because they have optimal security measures and comprehensive, specialized insurance coverage.

5. Compare Quotes

At this point, you should be ready to compare policies. If you’re storing gold at home or in a safety deposit box, the easiest solution may be to add a personal property rider to your existing policy.

If your existing policy’s rider option still doesn’t cover the full value, you will need to insure gold bullion with a standalone policy. This may require that you seek out a specialty insurance provider.

When storing precious metals in a depository or vault, the process will be more straightforward. Simply select the service package that includes the appropriate amount of coverage for your holdings.

6. Finalize With Caution

Now that you know how to insure gold, the final step is choosing a provider and plan that checks all the boxes and signing the papers.

Thoroughly read all contracts from front to end, and then read them again. Ask your insurance agent as many questions as needed until you’re 100% confident in your decision. Keep all documentation stored securely, ideally both physically and digitally.

Contact Us for a Free Consultation

As long as you insure bullion through a reputable insurance provider, you should have recourse available if your holdings are stolen, lost, or damaged. However, prevention is better than cure. Choose your storage method carefully.

Endeavor Metals is a Tier 1 precious metals dealer with over five decades of in-house experience. We’re standing by to provide personalized advice as you plan your precious metals investment.

Whether you’re investing in gold bars, gold coins, or gold numismatics, or opening a precious metals IRA, our team can provide expert guidance every step of the way.

Don’t navigate your gold investment alone. Contact us now for a free consultation on how to insure gold bullion based on your specific needs.

Contact Us Today!

Have a question? Call 855.753.3575 and speak with a live representative.